Cash Planning for Nonprofits

8 min read · Nonprofit Operations · Financial Planning

Welcome to Cash Flow Planning 101.

Nonprofits had a great year in 2025 — BDO recently reported that 86% of nonprofits saw increased revenue, and 90% of respondents also are projecting increased growth this year.

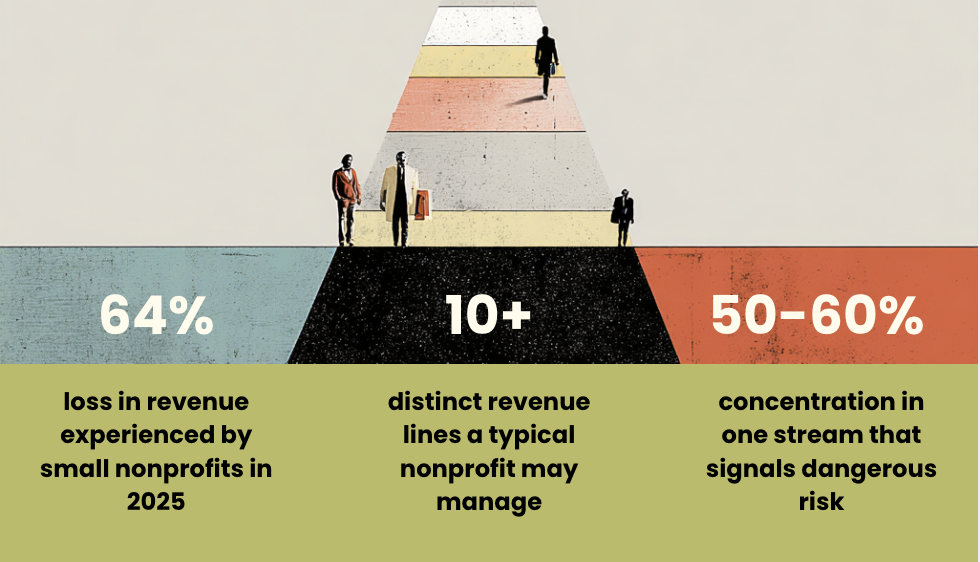

That’s incredible news for the sector. Even still, small to midsize nonprofits are underperforming compared to large nonprofits: Blackbaud recently reported 11.7% revenue growth YOY for large nonprofits, while medium-sized organizations grew more modestly at 2%. Small organizations saw losses of about 6.4% YOY, in large part due to less diversification in a moment when every nonprofit is subject to increased scrutiny (and receives less government funding).

An accurate, measured cash plan and forecast are a must for these organizations, and one of the first steps towards achieving resilience. Cash plans and forecasts streamline operational and growth decisions by showing exactly what’s possible—and what’s mission-critical. Without these key strategic tools, it’s all too easy to become overextended in an effort to launch that next campaign, or ramp up that new revenue stream, or expand your regional footprint.

That said, cash planning for nonprofits can be more complex than many other businesses. A typical small business might manage three or four revenue streams. A nonprofit can easily run ten — grants, endowments, investment income, events, major donors, recurring small donations, peer-to-peer campaigns, programmatic revenue, and more. Each one moves on its own calendar, its own cycle, its own logic. Stacking all of those cash flows on top of each other is where clarity — and good planning — begins.

We’re sharing our fundamental advice on nonprofit cash planning below. Let’s be real: you won’t learn how to create a functional cash plan in this article.

You can learn how to understand the process, and adjudicate your current plan and forecast. That puts you in a better position to vet a finance pro who can help.

1. Map every revenue stream on paper

The first step in creating a nonprofit cash plan is deceptively simple: start by writing down where the money comes from. Not in your head. On paper (or a spreadsheet), where you can actually see it.

For each stream, document the expected monthly amount and the timing. Small donations may be stable and predictable. A major annual gala is a single spike. Programmatic revenue could be consistent or lumpy depending on the program. When you layer all of these onto a single calendar view, patterns that lived only in a gut feeling suddenly become visible data. Executive directors often already know which months feel tight. The map confirms the intuition and gives the team something concrete to manage against.

As Sarah Jordan, Level CFO puts it, “It's literally putting it in black and white and getting the visual — that is the starting point. It’s finally understanding why September has always made you nervous, or why end of year feels so weirdly flush. Now you can see exactly when revenue hits, and start making strategic decisions accordingly."

2. Distinguish commitments from conversations

One of the most common and costly mistakes in nonprofit cash planning is treating interest as income. Someone mentions a donation at a gala. A foundation program officer sounds enthusiastic on a call. These feel real — but they aren't in the bank.

Key principle:Separate what you have a signed commitment for from what you have a promising conversation about. Only the former belongs in your cash plan.

Beyond the commitment question, think about control. An event you can market, price, and sell has levers you can pull. A major gift from a single donor does not — no matter how many conversations you have, the decision is ultimately theirs. Plan accordingly.

3. Diversify revenue — and resource it properly

Revenue diversification is standard advice: in our view, if any single revenue source represents 50–60% or more of total income, that’s too risky. A single bad year for that line of income can threaten the entire organization. A case in point: many organizations that relied on a single large annual event learned this lesson painfully during COVID-19 shutdowns, especially for those who didn’t have cancellation protection via contract.

But when you’re already feeling strapped, how do you execute on the need to diversify?

We like to start that conversation by asking this question: who is actually going to do the work to build a new stream? Is there capacity for current staff to do this work, do you need a new hire, or could a board committee take it on? Grant writing, for example, is often well-suited to a volunteer committee — search, write, and submit. Running a new paid program is not; it needs staff to deliver, market, and collect.

You don’t always need a brand new revenue stream to diversify your income. One easy approach: squeeze more from already-dependable events and programs. Consider what can be added to events already on the calendar — silent auctions, raffles, on-demand content from recorded sessions, sponsorships, educational add-ons, and merchandise sales.

4. Stay conservative on timing

We’ve all experienced it: revenue that you expect to come in Q3 slides to Q4; grants that feel certain take longer to process. Donor checks that were promised in November arrive in January. That’s why we often see nonprofit cash forecasts with inaccurate—and thus unhelpful—timing.

Honestly, the trick to timing is staying as conservative as possible. Here’s how we approach it:

We always track two numbers weekly: total revenue and weeks of cash on hand

Then, we start pulling levers 3–4 months before a projected shortfall — not when we are already against the wall

The next step is to build scenario assumptions that we can present clearly to the board

Then if leadership wants to invest aggressively, set a clear early indicator of success — and agree on it in advance

When presenting cash concerns to a board that wants to spend reserves, specificity wins. We always show three months of projected cash use side by side with projected revenue. There's very little subjectivity in a clear runway chart.

5. Know your emergency levers before you need them

Every organization should have a pre-established list of what to do if cash gets tight. And the time to think through this list is not during a crisis.

Priority #1 —Protect payroll above everything else. When staff hear that payroll is in jeopardy, turnover follows quickly — and in nonprofits where people are already working on tight budgets for mission-driven reasons, that trust is hard to rebuild.

Lines of credit and credit card flexibility should be mapped out in advance — including which cards have fixed limits and which have flexibility. Beyond credit, consider which operating costs can be temporarily deferred: rent deferrals can often be negotiated with landlords on a short-term basis without major consequences. Marketing spend can be shifted toward higher-return channels. Headcount reductions are a last resort and take the longest to implement.

The goal is to begin pulling available levers 3–4 months before a crisis, giving any corrective action on the revenue side enough time to take effect.

Cash planning isn't glamorous work, but it's the foundation everything else rests on. The nonprofits that thrive long-term aren't necessarily the ones with the most generous donors — they're the ones that can see what's coming, make decisions early, and protect their ability to operate when the unexpected happens. The five steps above won't build your cash plan for you, but they will give you a clearer picture of where you stand and what questions to ask. The most important takeaway? The earlier you take action to address cash issues, the more options you’ll have.

Most nonprofits don’t fail because their mission isn’t worthy, but rather because they run out of cash at the wrong moment. We’re not going to let that happen. Book a free consultation with a Level CFO today.